What is long-term care insurance?

Long-term care insurance provides funding for long-term care, including a nursing home or at-home care.

The bad news is that there are only a handful of companies that still offer long-term care insurance. If you’re able to find a policy, you’ll pay a lot more than someone a decade ago.

The reason why fewer companies offer long-term care insurance comes down to costs:

- People are living longer while getting long-term care. That means more money being paid out by insurers.

- Fewer people are buying long-term care policies, which means fewer dollars helping pay for those collecting benefits.

How do you get long-term care insurance?

The first step is to find an insurance company that offers long-term care policies.

You’ll also need a medical exam. The insurer will decide whether you’re a risk.

Younger people have a better shot at getting approval, so it's best to buy insurance young.

How much does long-term care insurance cost?

Long-term care policies can become expensive. State regulators are concerned about the rising costs, but insurers argue the rate increases are needed to help the changing market.

Specific long-term care insurance rates vary by age, health, level of benefits and insurer. Here are 2020 (the most recent data available) annual premiums for a $164,000 policy, according to the American Association for Long-Term Care Insurance:

- Single male, age 55 -- $1,700

- Single female, age 55 -- $2,765

- Couple, age 55 -- $3,050

What is combination life insurance?

Combination life insurance is a permanent life insurance policy with a long-term care insurance rider.

This rider allows you to tap into your long-term care savings if you need it. You don’t pay taxes on it. If you don’t use it, the money will go toward a death benefit.

You can add other riders to the policy like:

- Accelerated death benefits

- Disability income

- Critical illness

Once a doctor signs off, you get a percentage of the overall death benefit for the insurance rider. An example is if you have a $200,000 life insurance policy and a rider for 3% a month for long-term care, you could tap into $6,000 a month for long-term care expenses.

How much does combination life insurance cost?

Combination life insurance isn’t cheap.

A combination life insurance policy may cost you $75,000 if you’re willing to pay one lump sum for the long-term care rider. It may cost more if you spread out the payments over a few years. So, it’s not usually an option for someone who doesn’t have money available.

How do you get combination life insurance?

Unlike long-term care insurance, many insurers offer combination life insurance. If you already have a permanent life insurance plan, you can talk to your insurer about adding a long-term care rider or changing policies.

Since it’s a permanent life insurance plan, you can also add other riders to create a policy that works for you.

Once you find a policy for you, the insurer will likely ask a series of health-related questions and you’ll probably need a medical exam. The insurer will decide about approval and your rates by the answers to those questions and the exam.

Differences between long-term care insurance and combination life insurance

There are many differences between long-term care insurance and combination life insurance. Here are a few of them:

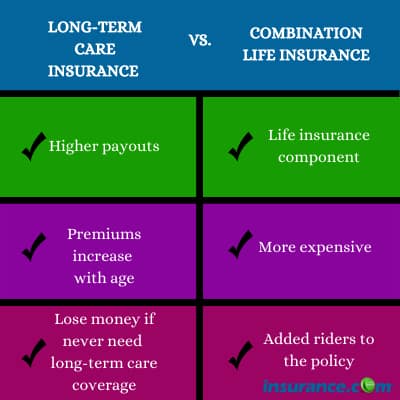

- Combination life insurance provides permanent life insurance as well as long-term care coverage.

- Long-term care insurance is only for long-term care.

- Combination life insurance is more expensive than long-term care insurance.

- Long-term care insurance premiums increase as you age. Combination life insurance premiums are usually consistent.

- You lose any money not spent on a long-term care insurance policy.

- Long-term care insurance usually has larger payouts than combination life insurance.

What long-term care plan is right for you?

It depends on your situation, finances and what you want out of your coverage.

Here are questions to ask yourself:

- What do you want out of a policy? Do you just want long-term care coverage or the ability to transform that money into a death benefit?

- How much money do you have to spend on a policy?

- Do you already have life insurance or do you need a policy?

- Do you have beneficiaries who need a death benefit?

- Are you OK with spending higher rates for long-term care insurance as you age?

The answers to those questions will help you figure out what’s a better choice.

Then, your next step is to talk to a financial planner. Create budgeting and financial modeling to figure out whether you need long-term care protection.

If you feel you need it, shop around and get quotes from multiple companies. You may want to price both long-term insurance and combination life insurance to see which avenue makes sense for you.

How do people pay for long-term care?

Medicare usually doesn’t cover long-term care. Medicare covers your medical expenses, but when it comes to long-term care, you’re generally on your own.

One exception is people who qualify for Medicaid. Medicaid will pick up a portion of the costs of long-term care.

However, if you don’t qualify for Medicaid, you’ll need to figure out a way to pay for long-term care. That could result in your family selling your home to help pay for nursing home care.

Long-term care can cost thousands a month, so having a plan to pay for it is important.

When can you use long-term care protection?

A doctor must diagnose you with cognitive impairment or deem you incapable of performing at least two of six daily living activities:

- Bathing

- Continence

- Getting dressed

- Eating

- Toileting

- Transferring (moving to and from a bed or a chair)

Once a doctor signs off, you’re able to submit claims for your long-term care. Once you get the OK for long-term care insurance, you, your family or your representative can file claims.

In case you missed it

Stay updated with our latest insurance insights and guides

You can get affordable long-term care insurance by shopping early and comparing...

Read articleLong-term care insurance helps pay for care at home, in assisted living,...

Read articleDisability insurance helps replace part of your income if you can't work...

Read article