What is the average cost of full coverage car insurance?

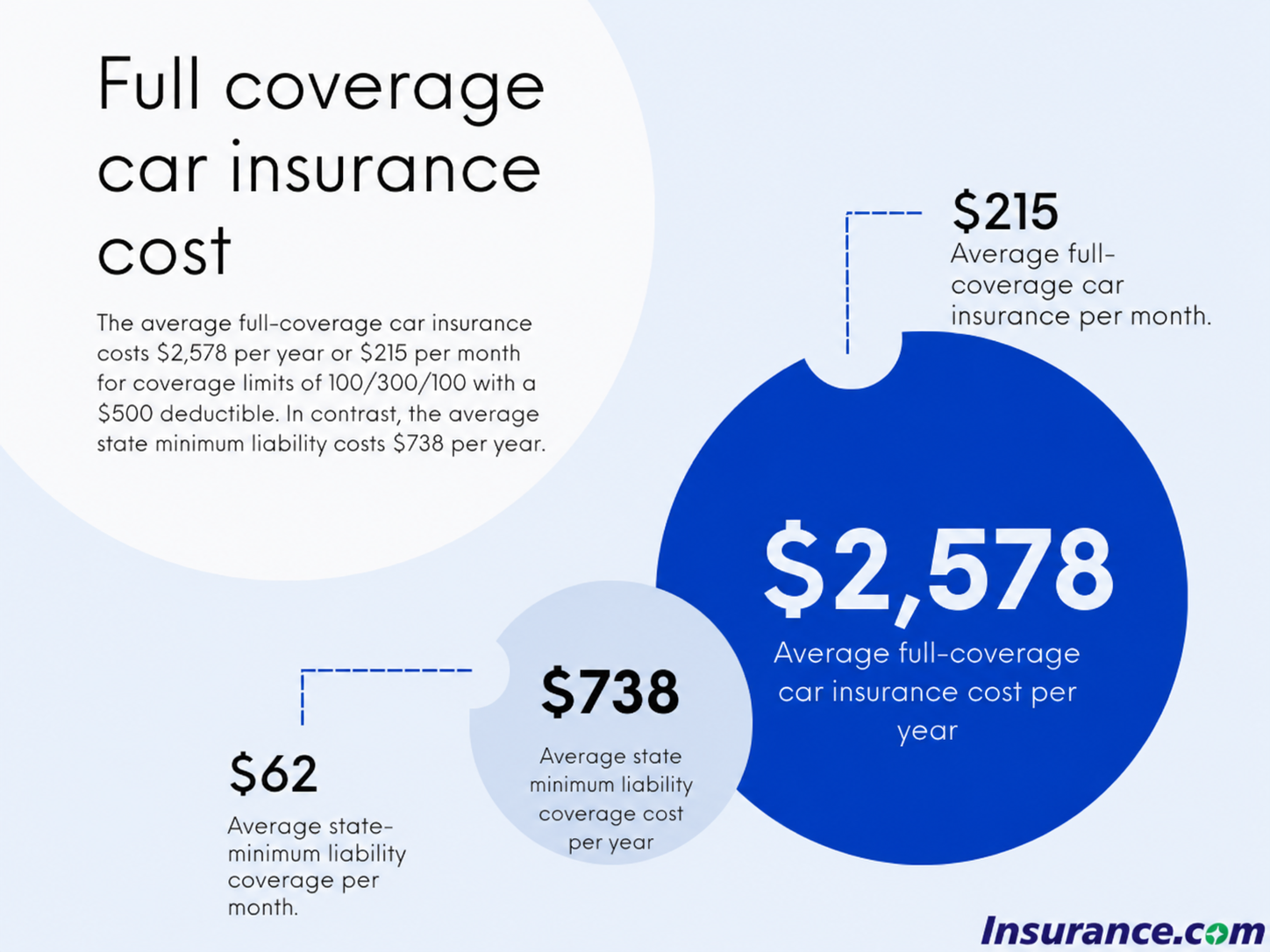

The average cost of full coverage car insurance is $2,578 per year, or about $215 per month. That’s based on liability insuranceLiability insurance covers sums that an insured becomes legally obligated to pay because of bodily injuries or property damage, or financial losses caused to other people. coverage of 100/300/100 ($100,000 per person, $300,000 per incident for injuries, and $100,000 for property damage) and $500 deductibles.

According to Insurance.com analysis (2026), Travelers has the cheapest full coverage car insurance rates, at $164 per month, or $1,962 annually, followed by GEICO and Nationwide. USAA offers cheaper insurance coverage to people who are eligible.

By comparison, the average cost of state minimum coverage is $738 annually. That amount:

- Provides the lowest level of liability coverage you can buy

- Doesn't provide any coverage for your car

Below you’ll find the cheapest national companies for full coverage auto insurance.

| Company | Average annual premium | Average monthly premium |

|---|---|---|

| Travelers | $1,962 | $164 |

| GEICO | $2,159 | $180 |

| Nationwide | $2,524 | $210 |

| Progressive | $2,569 | $214 |

| State Farm | $2,875 | $240 |

| Allstate | $3,159 | $263 |

| Farmers | $3,207 | $267 |

| USAA* | $1,628 | $136 |

*USAA only provides coverage to military members, veterans and their families.

People ask

How much is full coverage insurance on a new car?

The average car insurance rate for a full coverage policy on a new car depends on the car's make and model as well as personal factors like your driving record and where you live. Our average car insurance price is based on a 2024 Honda Accord LX.

How much is full coverage car insurance in your state?

Vermont is the cheapest state for full coverage car insurance, with an average car insurance cost of $1,660 annually. The three cheapest states are:

- Vermont: $1,660, $918 below the national average

- New Hampshire: $1,689, $889 below the national average

- Hawai'i: $1,757, $821 below the national average

Louisiana is the most expensive state for full coverage car insurance, at $3,999 annually. The three most expensive states for full coverage are:

- Louisiana: $3,999, $1,421 above the national average

- Michigan: $3,964, $1,386 above the national average

- Nevada: $3,963, $1,385 above the national average

Full coverage car insurance covers different things depending on your state, because state minimum requirements vary. Below you’ll find how much full coverage costs in each state.

| State | Average annual rate | Average monthly rate |

|---|---|---|

| Alabama | $2,116 | $574 |

| Alaska | $2,167 | $588 |

| Arizona | $2,420 | $768 |

| Arkansas | $2,942 | $689 |

| California | $3,444 | $897 |

| Colorado | $3,181 | $651 |

| Connecticut | $2,742 | $1,048 |

| Delaware | $3,157 | $1,300 |

| Florida | $3,916 | $1,228 |

| Georgia | $2,503 | $860 |

| Hawaii | $1,757 | $477 |

| Idaho | $1,901 | $594 |

| Illinois | $1,938 | $527 |

| Indiana | $1,894 | $506 |

| Iowa | $2,460 | $481 |

| Kansas | $2,496 | $698 |

| Kentucky | $2,624 | $721 |

| Louisiana | $3,999 | $1,033 |

| Maine | $1,808 | $469 |

| Maryland | $1,999 | $810 |

| Massachusetts | $2,429 | $789 |

| Michigan | $3,964 | $1,303 |

| Minnesota | $2,591 | $852 |

| Mississippi | $2,397 | $628 |

| Missouri | $2,151 | $563 |

| Montana | $2,476 | $521 |

| Nebraska | $2,095 | $515 |

| Nevada | $3,963 | $1,212 |

| New Hampshire | $1,689 | $567 |

| New Jersey | $3,122 | $1,395 |

| New Mexico | $2,577 | $562 |

| New York | $2,596 | $1,279 |

| North Carolina | $2,638 | $681 |

| North Dakota | $2,439 | $564 |

| Ohio | $1,783 | $475 |

| Oklahoma | $2,993 | $585 |

| Oregon | $2,048 | $834 |

| Pennsylvania | $2,327 | $460 |

| Rhode Island | $2,878 | $845 |

| South Carolina | $2,417 | $785 |

| South Dakota | $2,575 | $450 |

| Tennessee | $2,235 | $613 |

| Texas | $3,106 | $841 |

| Utah | $2,356 | $850 |

| Vermont | $1,660 | $392 |

| Virginia | $1,835 | $693 |

| Washington | $2,389 | $638 |

| Washington, D.C. | $3,465 | $918 |

| West Virginia | $2,415 | $587 |

| Wisconsin | $2,343 | $569 |

| Wyoming | $2,061 | $339 |

How much is full coverage car insurance by age?

Based on Insurance.com rate data (2026), full coverage car insurance for new drivers is more expensive than for older drivers; Nationwide is the cheapest at 16 ($6,094), while Travelers is the cheapest at 17 ($5,117), 18 ($4,296) and 19 ($3,476). At age 25, Nationwide is again the cheapest ($1,831), and remains the cheapest at all other ages in our data set. Rates continue to decline until about age 65, where Nationwide's average rate is $1,372 and Allstate's is $2,352.

- At 16, Nationwide has the cheapest average rates at $9,725 a year; Progressive charges

$9,297 - At 17 through 19, Travelers has the cheapest rates ($5,117, $4,296, $3,476, respectively); Farmers is the most expensive at 17 ($9,030) and 18 ($7,903), while Allstate is the most expensive at 19 ($5,170)

- At 30, Nationwide is still the cheapest at $1,626 a year; State Farm charges $2,055

- At 55, Nationwide's rate is $1,380 a year; Allstate charges $2,314

Take a look at the average cost of full coverage car insurance by age below.

| Company | Average annual rates |

|---|---|

| GEICO | $8,436 |

| Travelers | $9,142 |

| State Farm | $9,558 |

| Nationwide | $9,725 |

| Progressive | $12,799 |

| Allstate | $12,863 |

| Farmers | $18,034 |

| USAA | $8,080 |

*USAA offers coverage only to military members, veterans and their families.

What are the best companies for full coverage car insurance?

Data from Insurance.com indicates (2026), Travelers is the best full coverage car insurance company, with a 4.55 overall Insurance.com score, followed by GEICO and Nationwide, with scores of 4.5 and 4.19, respectively.

Below is a full list of the top insurance companies for full coverage based on price, NAIC complaint ratio, customer satisfaction and AM Best financial ratings. The overall Insurance.com score is calculated out of five using these factors.

| Company | Overall score | Average annual premium | Customer satisfaction survey score | AM Best rating |

|---|---|---|---|---|

| Travelers | 4.55 | $1,962 | 4.37 | A++ |

| GEICO | 4.5 | $2,159 | 4.27 | A++ |

| Nationwide | 4.19 | $2,524 | 4.41 | A |

| Progressive | 4.05 | $2,569 | 4.15 | A+ |

| Amica | 4.02 | $2,769 | 4.19 | A+ |

| State Farm | 3.91 | $2,875 | 4.38 | A+ |

| Allstate | 3.57 | $3,159 | 4.35 | A+ |

| Farmers | 3.52 | $3,207 | 4.3 | A |

| Auto-Owners | 4.55 | $2,173 | 4.3 | A+ |

| Erie | 4.5 | $1,967 | 4.5 | A |

| American Family | 4.44 | $2,665 | 4.27 | A |

| Auto Club Group (AAA) | 4.3 | $1,834 | 4.39 | A |

| Auto Club of Southern California (AAA) | 3.76 | $3,507 | 4.48 | A+ |

| CSAA Insurance Group (AAA) | 3.68 | $3,008 | 4.37 | A |

| Mercury | 3.56 | $3,107 | 4.46 | A |

In our rankings, full coverage includes liability limits of 100/300/100 and $500 deductibles.

People ask

Which company has the cheapest full coverage car insurance?

Travelers has the cheapest full coverage auto insurance rates among national carriers at $1,962 a year or $164 a month. USAA is cheaper at $1,628 a year, but is only open to military members, veterans and their families.

How do you decide if you need full coverage car insurance?

You need full coverage car insurance if your vehicle is financed or leased; your lender will require it. You should also carry full coverage if you cannot afford to repair or replace your car out of pocket, or if your car is new or high-value. You can consider dropping to liability-only if your car is paid off, its market value is low and you have savings to cover repair or replacement.

You should pay extra for full coverage if:

- You have a loan or lease on your car (it will be required)

- You can't afford to repair or replace your car out of pocket

- You have a newer car that would be expensive to repair or replace

- You simply want peace of mind

You can save the money and buy liability-only if:

- You own your car outright

- You have an older, low-value car

- You have the savings to replace or repair your car

What affects the cost of full coverage car insurance?

The cost of full coverage insurance is most influenced by your vehicle's make, model, and trim level, your driving record, your age, and where you live. With full coverage, unlike liability-only, the vehicle's value matters because the insurance company is covering the cost of repairing or replacing it.

| Factor | Why it matters for full coverage |

|---|---|

| Vehicle make, model and trim level | A car with a higher value costs more to repair or replace |

| Age* | Younger drivers are at a higher risk of an accident |

| Driving record | Drivers with tickets or accidents are a greater risk for a claim |

| Gender** | Male drivers are more likely to cause an accident, especially younger ones |

| Location | State law, weather, crime and traffic rates all impact claim rates |

| Credit history*** | Credit is statistically correlated with the likelihood of filing a claim |

| Annual mileage | More time on the road increases the chances of an accident |

*Cannot be used in Hawai'i and Massachusetts

**Cannot be used in California, Hawai'i, Massachusetts, Michigan, Montana, North Carolina and Pennsylvania

***Cannot be used in Hawai'i, California, Massachusetts and Michigan

Use our online car insurance calculator to get a personal recommendation for what kind of car insurance coverage you should buy and what deductibles to consider.

How can you get cheap full coverage car insurance?

To find the cheapest full-coverage car insurance, shop around and compare quotes, raise your deductibleThe deductible is the amount you pay out of pocket for a covered loss when you file a claim., ask about discounts and bundle your auto insurance with your home or renters insurance with the same carrierAn insurance carrier is the company that provides your car insurance policy and pays claims..

- Raise your deductible. A higher deductible is the easiest way to get lower rates, but make sure you can afford it if you need to pay it.

- Bundle your coverage. You can save on your car and home or renters insurance when you buy from the same company.

- Ask about discounts. There are dozens of possible car insurance discounts available, so make sure you’re getting everything you qualify for.

Methodology

Rate data is sourced through Quadrant Information Services and fielded across all 50 states and Washington, D.C. covering 34,588 ZIP codes.

Unless otherwise indicated, averages are based on our full coverage data set. This data set is based on:

- Bodily injury liability of $100,000 per person and $300,000 per incident

- Property damage liability of $100,000 per incident

- Comprehensive and collision deductibles of $500

- 40-year-old driver

- Honda Accord LX

- Good credit

- A clean driving record

- 12-mile commute, 10,000 annual mileage

Additional rate data is drawn based on:

- Ages ranging from 16 to 75

Best insurance company scores are based on Quadrant rates as well as:

- Customer satisfaction scores from our annual survey of insurance consumers

- National Association of Insurance Commissioners Complaint Index, where a score of 1.00 is considered average.

- AM Best financial stability ratings, which range from D to A++

Learn more about our methodology and data.

FAQ: Full coverage car insurance cost

How much is full coverage insurance on a used car?

As with a new car, the cost of full coverage auto insurance depends on the year, make and model, current market value. Older, lower-value cars are cheaper to insure than newer ones. The average cost of insurance on a 2024 Honda Accord LX is $2,578; rates for a lower-value car will be lower if all other factors remain equal.

How much is full coverage insurance a month?

Full coverage car insurance costs an average of $215 a month nationally. Rates range from $136 a month with USAA (for eligible military families) to $267 a month with Farmers. Travelers is the cheapest national carrier open to everyone at $164 a month.

Do you have to have full coverage insurance when financing a car?

Yes. If you are financing your vehicle, your lender will require you to carry full coverage to protect its investment in the vehicle.

Is full coverage car insurance worth it?

As with all insurance, full coverage is worth it if you need to use it. If you can't afford to repair or replace your car, full coverage car insurance is worth having.

When should you drop full coverage on your car?

Consider dropping full coverage when your car loan is paid off and your car's market value is low enough that the annual cost of comprehensive and collision coverage approaches or exceeds the car's actual cash valueActual Cash Value (ACV) is the current market value of your car, considering depreciation. It's the amount your insurance will pay if your car is totaled or stolen., which is what you would receive in a total loss payout. A common rule of thumb: if the annual cost of comprehensive and collision is more than 10% of the car's actual cash value, dropping the coverage may make financial sense.

In case you missed it

Stay updated with our latest insurance insights and guides

Many factors are playing into higher car insurance rates, including inflation, more...

Read article