Pros and cons of an umbrella insurance policy

Umbrella insurance offers liability protection starting at $1 million at a relatively low cost, but it requires higher underlying policy limits and does not cover every type of loss.

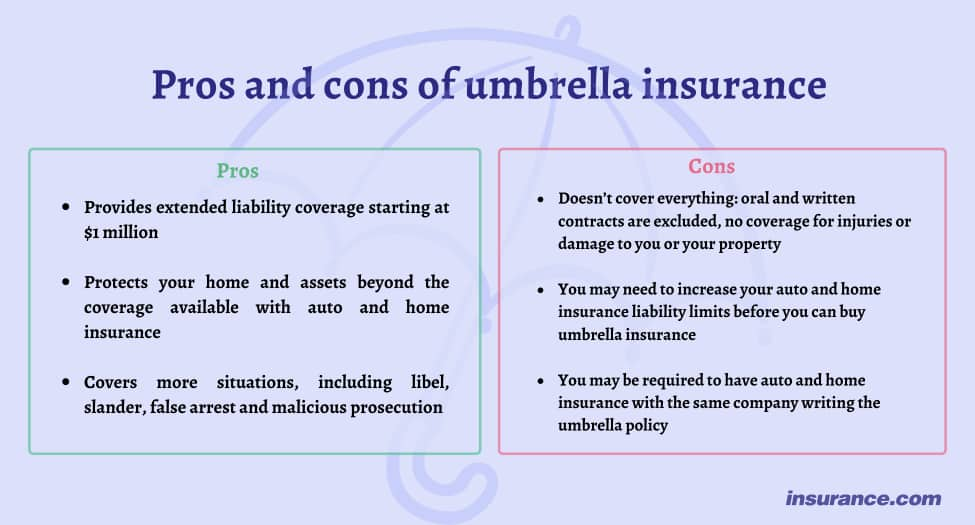

Pros

- Umbrella insurance provides liability coverage starting at $1 million, at a cost that is low relative to the amount of coverage.

- An umbrella policy helps to protect your assets, including your home, if you’re found to be liable or negligent for injuries or damage.

- Umbrella insurance starts where your home or auto coverage leaves off, meaning it’s an additional limit on top of that limit, creating a much larger pool of resources in a lawsuit or claim.

- Umbrella insurance covers liability types excluded from home and auto policies, including libel, slander, malicious prosecution and false arrest.

Umbrella insurance supplements rather than replaces existing liability coverage, activating only after your home or auto policy limits are exhausted. As Patrick A. Cozza, executive in residence at Silberman College of Business, Fairleigh Dickinson University, notes, umbrella insurance is low-cost relative to the amount of coverage it provides.

"The benefits of umbrella insurance are to offer additional liability protection beyond what you might have under your auto and/or homeowners policies. Umbrella insurance is a relatively low-cost insurance, relative to the amount of coverage," Cozza said.

Cons

- Umbrella insurance doesn’t cover everything; it doesn’t cover personal property, your injuries, written or oral contracts, war or terrorism or business losses, for example.

- Most umbrella insurers require you to carry the highest available liability limits on your home and auto policies before you can purchase an umbrella policy, which increases your total insurance cost.

- You may have to buy umbrella insurance through the same insurer as your home and auto; if your current company doesn’t offer it, that might mean switching.

People ask

What are the disadvantages of umbrella insurance?

The two main disadvantages of umbrella insurance are the added premiumThe payment required for an insurance policy to remain in force. Auto insurance premiums are quoted for either 6-month or annual policy periods. cost and the requirement to carry the highest available liability limits on your underlying home and auto policies. Umbrella insurance also does not cover every loss type, excluding personal property damage, your own injuries, contract disputes, war, terrorism and business losses.

Do you need an umbrella insurance policy?

You need umbrella insurance when your net worth exceeds the maximum liability limits available on your home and auto policies. If a judgment against you could exceed those limits, umbrella insurance protects the difference, covering your assets and future income.

Liability claims can exceed home and auto policy limits, leaving the policyholder personally responsible for court costs and judgments. This risk applies regardless of net worth, since future income can also be subject to a judgment.

To determine whether umbrella insurance is right for you, compare your total net worth and future income against your current home and auto liability limits. Get quotes from multiple insurers, as umbrella premiums and underlying limit requirements can vary by company.

"Like most insurance, it's best to shop around for the lowest premium," Cozza said.

Got a question about insurance? Our verified experts are here to help.

Verified expert advice and trusted by 50,000+ users

Verified expert advice and trusted by 50,000+ usersFAQ: Umbrella insurance

Is umbrella insurance worth it?

Umbrella insurance is worth it when your net worth or future income exceeds the maximum liability limits on your home and auto policies. It is also worth considering if you own property, employ household staff, have teen drivers, or regularly host guests, all of which increase your liability exposure.

When should you buy umbrella insurance?

Buy umbrella insurance when your total assets exceed the maximum liability limits available on your home and auto policies. For example, if your homeowners policy caps liability at $300,000 and your net worth is $500,000, a single lawsuit could expose $200,000 in unprotected assets.

Who needs umbrella insurance?

You need umbrella insurance if your total assets exceed the maximum liability limits on your home and auto policies. People with significant assets, teen drivers, rental properties, pools, trampolines or frequent social gatherings face higher liability exposure and are the most likely to benefit.