Pros and cons of umbrella insurance

There are both pros and cons to buying an umbrella insurance policy, although for most people the benefits outweigh the disadvantages. Umbrella insurance covers much more than either your auto or home insurance, but there are some caveats.

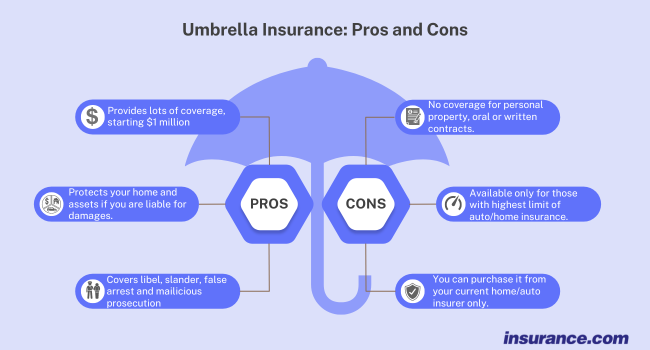

Pros

- Umbrella insurance provides a lot of coverage, starting at $1 million, for a low cost.

- An umbrella policy helps to protect your assets, including your home, if you’re found to be liable or negligent for injuries or damage.

- Umbrella insurance starts where your home or auto coverage leaves off, meaning it’s an additional limit on top of that limit, creating a much larger pool of resources in a lawsuit or claim.

- Umbrella insurance covers things home and auto don’t, like libel or slander, malicious prosecution and false arrest.

Cons

- Umbrella insurance doesn’t cover everything; it doesn’t cover personal property, your injuries, written or oral contracts, war or terrorism or business losses, for example.

- Generally, you can’t buy umbrella insurance unless you buy the highest available amount of home and auto liability protection, which means your home and auto insurance rates will be higher.

- You may have to buy umbrella insurance through the same insurer as your home and auto; if your current company doesn’t offer it, that might mean switching.

Should you buy umbrella insurance?

Anyone with a high net worth should buy umbrella insurance, but if you’re not sure, it’s best to consult with a financial advisor. Liability claims can easily exceed auto and home policy limits, and those with a lower net worth may be less able to handle additional court costs or judgments.

However, there are costs involved in buying more coverage, so take the time to be sure it’s right for you. "Like most insurance, it's best to shop around for the lowest premium," Cozza says.