Do states set car insurance rates by law?

No, but how car insurance rates can be set is regulated by the states. Companies set their own rates in accordance with state laws that prevent discrimination; each company must charge the same rate to drivers with the same risk profile, and they can't use prohibited characteristics like race or religion, and, in some states, age and gender. Here's how state regulation of insurance rates works.

- State laws ensure that a company charges the same rates to drivers who fit the same risk profile. That still allows companies to compete by setting rates for that profile that may be lower than a competitor's.

- Insurance companies are prohibited from using certain characteristics in setting their rates. Race and religion are among those factors. California, Hawaii, and Massachusetts prohibit the use of your credit information, and other states don’t allow the use of age or gender.

- States set the minimum levels of required insurance coverage. All except New Hampshire require drivers to buy insurance, and the amount of coverage required affects the cost of a basic policy.

How car insurance rates are calculated: A detailed look

Rates are calculated first by sorting each applicant into a group by age, location and risk profile, determining the base rate for all people in that group. From there, your rate is adjusted based on your vehicle and driving history; any discounts you qualify for are then deducted to finalize the rate. After you accept the quote, full underwriting takes place. If anything new is discovered, like a ticket or claimAn insurance claim is a request you make to your insurance company for coverage after your car is damaged or you have an accident. You can file a claim online, by phone, or in writing. you didn't disclose, your final rate may change. At this point, your credit may also impact the final rate, if you didn't provide a SSN for the quote.

Here are the steps to calculating a car insurance rate:

- You are sorted into a group. For example, married drivers in your ZIP code over age 25. This determines the base rate.

- The insurance company calls up the pricing information for that group. This is the same for all people who fit that profile. From here, things will be personalized further.

- Information about your vehicle is considered. Your car's year, make and model, its safety ratings, claims and crash history related to that vehicle: all of these things affect the base rate.

- Your driving history is reviewed. In a rate quote, the information you provide will be used as the basis for this portion of the rate.

- Any discounts you qualify for are subtracted from the price. The information you provide will help the insurer determine which discounts to apply.

- The insurance company will pull your driving record. It will consider its "lookback period", which is the number of years back the company considers tickets and accidents. That's commonly three years, but may be longer.

- Your claims history will be examined. Insurance companies have shared records of claims that are considered in rating.

- Your credit history will be reviewed. In most states, insurance companies can use credit history for rating. This is a soft pull (it doesn't affect your credit) and not the same as a FICO score. Some carriers may request this earlier in the process to prevent rate surprises.

If anything is found in the underwriting process that is different from what you entered in your quote request, it could change the final rate you pay. While the order of these steps may vary, the basics remain the same: A base rate is determined and then adjusted using surcharges and discounts.

How car insurance rate calculations work: An example

Sasha is a 32-year-old single woman in Pittsburgh who works from home. She applies for a full coverage car insurance policy for her 2021 Honda CR-V.

- Sasha is grouped by her base profile: Her ZIP code, age, gender and marital status.

- Sasha's vehicle is considered: Her 2021 Honda CR-V's safety record, value and repair costs. A base rate for Sasha's profile and vehicle are set at $1,200 a year.

- Sasha's credit is checked: Her good credit history reduces her base rate to $1,050.

- Sasha's driving record is reviewed: She was in a small, at-fault accident two years ago. A surcharge for this accident increases her base rate to $1,250 a year.

- Sasha qualifies for several discounts and rate reductions: Discounts are applied for low annual mileage, automated payments, paperless billing and for the anti-theft device installed on her car. The base rate is reduced to $1,110.

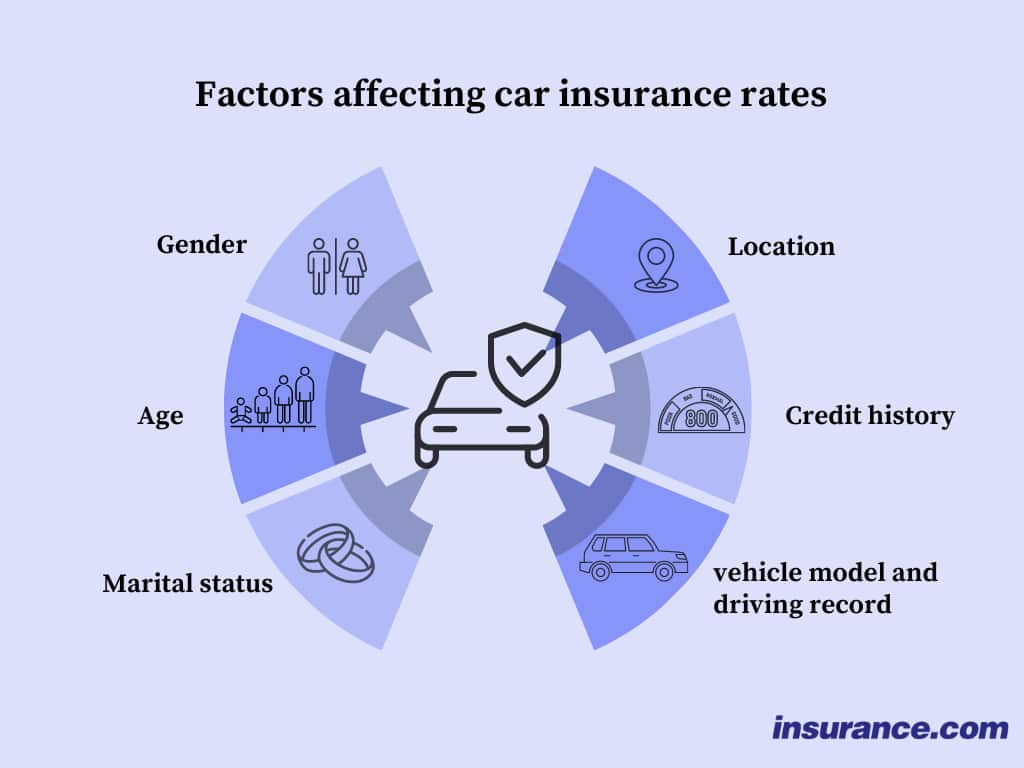

What are the factors that affect how much you pay for car insurance?

The factors that affect how much you pay for car insurance are your location, age, gender and other demographics, your driving record, your credit history, the make and model of your vehicle and the coverage you buy. A few states ban or limit the use of credit, age and gender.

- Demographics. Age, gender, marital status, ZIP code, number of years you’ve been licensed, homeownership, occupation, education and even grades

- Your driving record. Accidents, traffic violations, insurance history and past claims

- Your credit history. In most states, credit can be used a factor due to its correlation with risk of filing a claim.

- Your car and how you use it. Owned or financed, current value, annual mileage, claims record for all owners of that model, anti-theft devices and safety features, whether you use the car for business.

- How much coverage you buy. Liability limits, whether or not you buy comprehensive and collision (both of which carry a deductible that influences their final cost), medical payments, uninsured motorist, or extras such as rental reimbursement or towing.

Which factors affect car insurance rates the most?

For most drivers, location, age, driving history, credit and vehicle type have the biggest impact on rates.

Your ZIP code. Even if you have never filed a claim, your rate can increase dramatically simply by moving from one ZIP code to another.

Your age. Drivers with less than 10 years of experience pay more. The less experience you have, the worse the penalty. Brand-new drivers can pay an additional surchargeAn increase in your auto insurance premium due to an at-fault accident or a moving violation. Learn more about how a surcharge affects your auto insurance premiums. on top of that.

Your driving record. Claims tend to matter more than speeding tickets do. More than one of either is bad news, and so is a major violation such as a DUI.

Your credit. Insurance companies point to numerous studies that correlate poor credit scores with higher numbers of claims. The flip side: When your credit improves, your rates should decrease.

Your previous insurance coverage. If you are not currently insured, you are likely to pay much higher rates for at least your first term.

Why do insurance companies have such different rates?

Insurance company rates differ because each company has many different basic rate groupings and can set different prices for those groups, basing its estimate of risk on the number and cost of claims that group has filed in the past. Then the company applies its own surcharges and discounts based on factors specific to a particular driver. Each carrier determines how much weight it places on each factor; with higher rates for risk pools the carrier prefers to limit.

For example, a carrier that wants to limit its exposure in the teen driver market may price teen drivers much higher, encouraging them to seek coverage elsewhere.

In case you missed it

Stay updated with our latest insurance insights and guides

Compare car insurance companies from multiple angles to find the best price,...

Read articleThe car insurance declarations pageThe declarations page of your policy includes important details like the name, description, and location of the insured property, the policyholder's name and address, the coverage period, the premiums and the coverage amount. It's also called a 'dec page' or 'dec sheet.' outlines your policy's coverage and limits, as...

Read articleModified car insurance provides coverage for additions or changes made to a...

Read articleThe main types of car insurance are liability, comprehensive and collision, uninsured/underinsured...

Read articleMost states have laws requiring the minimum amount of auto insurance you...

Read articleFactors like your age, driving record, coverage, location and vehicle impact car...

Read articleParked car insurance, or storage coverage, is comprehensive-only coverage that prevents a...

Read articleClassic car insurance is an agreed-value policy designed for classic, antique, and...

Read articleTo cancel your auto insurance, contact your insurer, request cancellation, provide written...

Read articleEstimate your insurance costs with our used car insurance calculator using vehicle...

Read article